یہ بھی دیکھیں

12.06.2026 12:49 AM

12.06.2026 12:49 AM

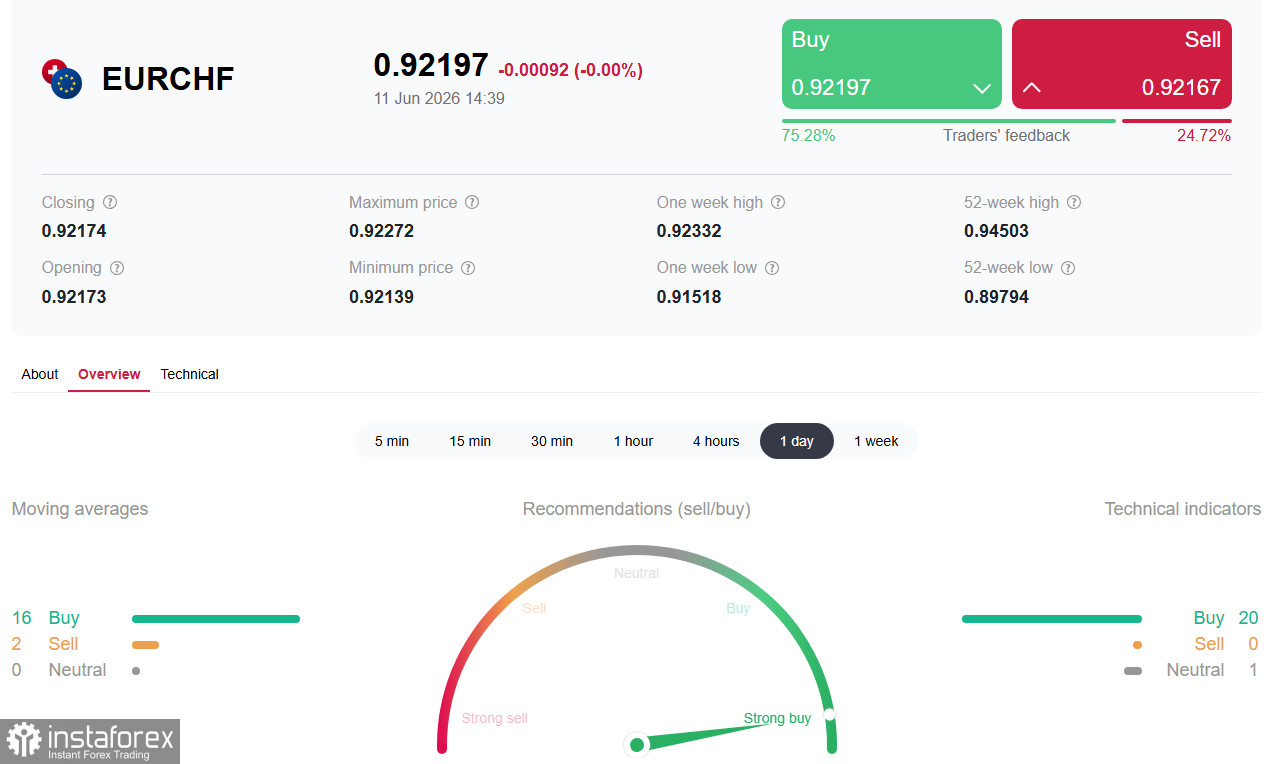

The EUR/CHF cross entered midweek with a confident rise, trading around 0.9220–0.9230 after bouncing off early-June lows of about 0.9130. The pair is exhibiting a stable upward trend amid a key divergence in the monetary policies of the European Central Bank (ECB) and the Swiss National Bank (SNB).

Unlike many other currency pairs dominated by the US dollar, the dynamics of EUR/CHF are shaped by two unique factors: on one hand, the ECB is raising rates for the first time since September 2023 amid an energy inflation shock; on the other hand, the Swiss National Bank continues to rely on currency interventions as the primary tool for containing inflation and maintaining the competitiveness of the Swiss economy.

On June 11, the European Central Bank announced a 25-basis-point increase in key interest rates, as expected. Consequently, the rate for main refinancing operations, the marginal lending facility, and the deposit facility now stand at 2.4%, 2.65%, and 2.25%, respectively.

Although the rate hike was widely anticipated by the markets, an important signal was that ECB President Christine Lagarde maintained a cautiously hawkish tone, acknowledging the risks of further inflationary pressure from rising energy prices. This allowed markets to maintain expectations of a possible second rate hike in the coming months.

In contrast to the ECB, the SNB is in a completely different situation. Inflation in Switzerland remains low, allowing the SNB to keep its key interest rate at 0.00% (and not consider raising it). Instead, the primary tool is currency interventions.

Since the last meeting, statements from SNB representatives have emphasized the bank's increased readiness to intervene in currency markets. Chairman Schlegel (on June 3) noted that "the war in Iran could increase pressure on the franc," and the SNB has "heightened its readiness for currency market interventions."

The current divergence in policies creates classic prerequisites for the euro to strengthen against the franc. All of the above should support EUR/CHF around 0.9200, with a possible move towards 0.9300 in light of the ECB meeting's outcomes.

The Swiss franc is traditionally considered one of the major "safe-haven assets" alongside gold. However, the current conflict in the Middle East demonstrates a paradoxical dynamic.

| Thursday, June 11 (12:45 GMT) | Press conference of ECB President Christine Lagarde | Anticipated signals on future steps | Primary source of volatility on Thursday |

| Thursday, June 11 (12:30 GMT) | US PPI Data (Producer Price Index) | Actual: 6.5% YoY (maximum since 2022) | Indirect impact via the US dollar |

| End of June | Publication of SNB intervention data for Q1 | Expected increase in interventions | Important signal about SNB intentions |

| Throughout the Week | Statements from US, Iran, Israel Leaders | — | — |

The EUR/CHF cross is at the epicenter of the divergence in monetary policies between the ECB and the SNB. On one hand, the ECB raised rates for the first time since September 2023 and is likely to maintain a cautiously hawkish tone, with markets pricing in three hikes over the next 10-12 months. On the other hand, the SNB remains at the zero rate (0.00%) and is betting on currency interventions rather than rate hikes to curb inflation and support export competitiveness.

The interest rate differential (200+ bps) is a key driver of the pair's growth. An additional factor supporting the euro is the ECB's "cautiously hawkish" signal, which allows markets to maintain expectations of further tightening.

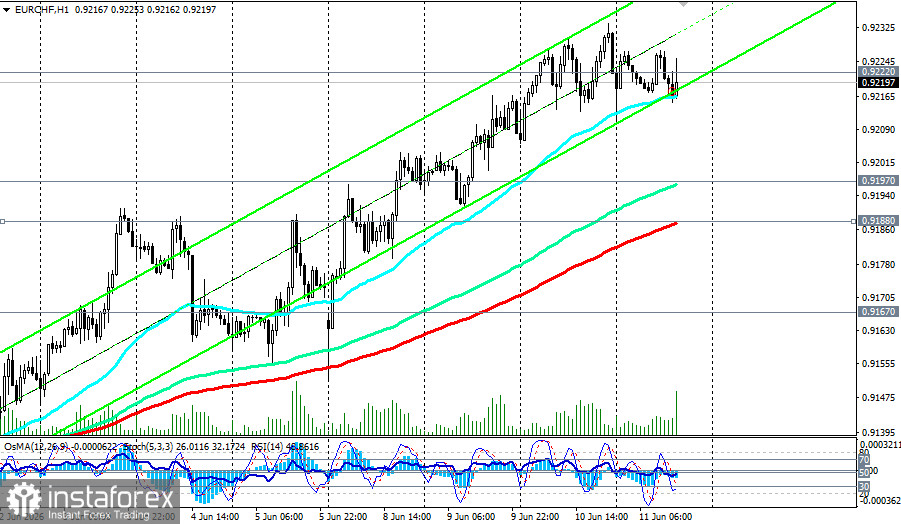

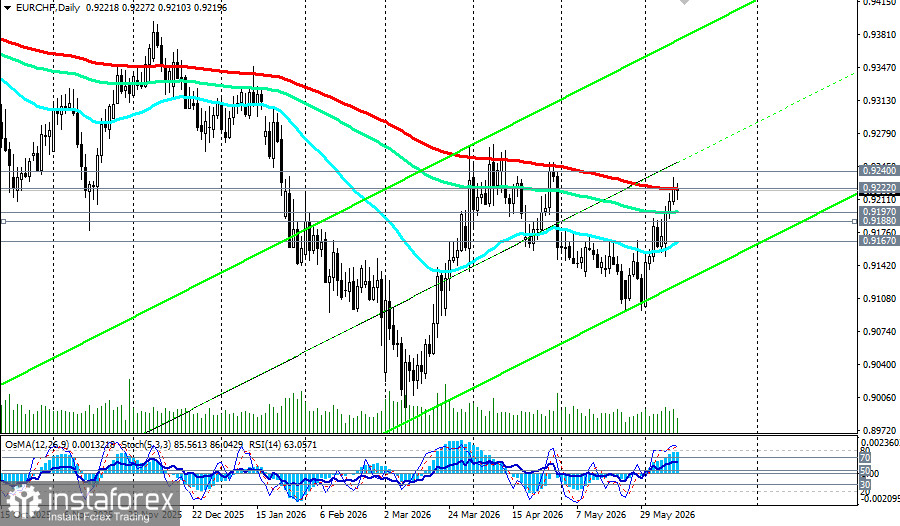

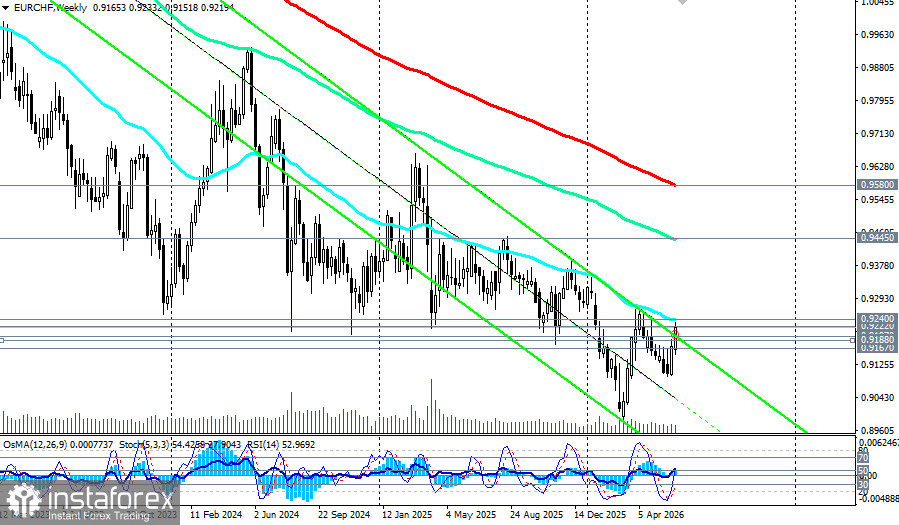

The key zone of 0.9197 (EMA144 on the daily chart)–0.9240 (EMA50 on the weekly chart) will become the arena for a decisive battle in the coming days.

A technical breakout below this level could trigger a short-term correction to 0.9170-0.9130, but fundamental factors (interest rate differential, hawkish ECB) indicate that the likelihood of a rise above remains.

Traders should exercise caution and closely monitor further statements from representatives of both central banks, the SNB's upcoming intervention data (end of June), and geopolitical developments in the Middle East.