আরও দেখুন

28.04.2026 02:05 PM

28.04.2026 02:05 PM

See also: InstaTrade trading indicators for WTI (CL)

Global oil prices continued to rise for a second session in a row, and have settled near multi-month highs. In the early hours of the European session on Tuesday, futures for West Texas Intermediate (WTI) traded around $99.00–$100.00 per barrel, while benchmark Brent exceeded $104.00. The main reason for the rally is the ongoing blockade of the Strait of Hormuz, which has cut access to the global market by roughly 14 million barrels per day, and the complete absence of progress in peace talks between the US and Iran.

Fundamental backdrop: physical shortage replaces hopes

Last week's optimism about a swift diplomatic resolution has evaporated. Over the weekend, US President Donald Trump cancelled a planned trip by his envoys to Pakistan, saying that Tehran's new proposal, although "better" than the previous one, was still "not good enough."

The White House confirmed it had discussed Iranian initiatives, but showed no readiness to accept them. Iran, in turn, conditions talks on the prior lifting of the maritime blockade, which makes the resumption of meaningful dialogue in the near term unlikely. For traders, the decisive factor is not rhetoric, but the physical flow of oil, and that flow remains severely constrained, say oil market analysts.

Ship-tracking data and expert estimates indicate that since the start of the conflict, roughly 850 million barrels of oil have effectively disappeared from the market. Up to 14 million barrels per day are not passing through the strait, even though minimal traffic continued after the blockade began.

New developments worsen the picture: six Iranian tankers were forced to turn back because of the US blockade, and only a handful of vessels, such as a UAE LNG tanker, have been able to transit. It has also emerged that Israel has expanded its strike zone over Lebanon, adding the risk of the conflict spreading to new regions.

This has changed experts' expectations: hopes for a restoration of supplies in April were not realized, and the likely reopening of the strait has been pushed out to May–June, with volumes expected to recover slowly. Moreover, low inventory levels and the need to replenish strategic stocks will keep prices elevated for a long time, even after shipping is unblocked.

The physical blockade has forced major investment banks to substantially revise their price forecasts upwards.

New oil forecasts (quarterly, selected banks)

| Bank | Outlook for Brent (Q2, 2026 ) | Outlook for WTI (Q2, 2026 ) | Key conditions |

| ING | $104/barrel | ($98-100 /barrel | Supply recovery from May |

| Citi (base) | $110 /barrel. | – | Recovery by end-May |

| Citi (bullis) | $150/barrel | – | Blockade persists until end-June |

| Goldman Sachs | $90 /barrel. (Q4) | $83 /barrel (Q4) | Normalization by end-June |

As the table shows, even in base scenarios banks expect Brent to remain well above $100 in the short term.

Citi, for example, outlines a "super-bullish" scenario with Brent at $150 if the strait stays closed until the end of June, mirroring peaks seen in past energy crises. At the same time, Citi analysts note that the current rally has been relatively restrained: prices have not surged as much as some expected, because the market spent too long hoping for a quick diplomatic solution. However, once the physical shortage becomes obvious, the correction could be rapid.

Brief technical analysis

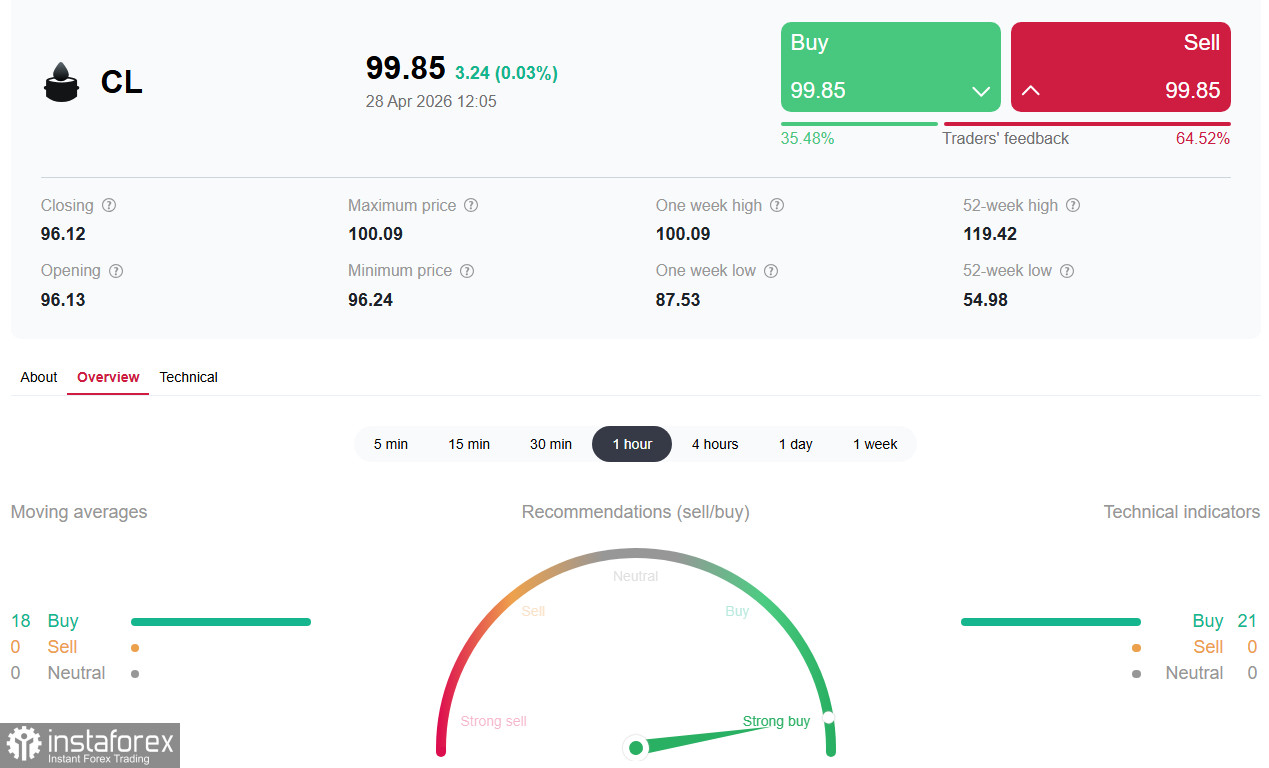

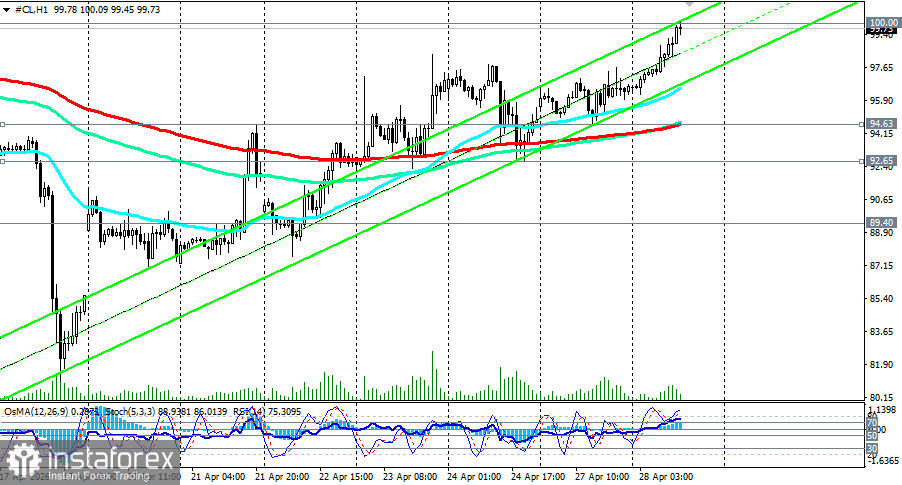

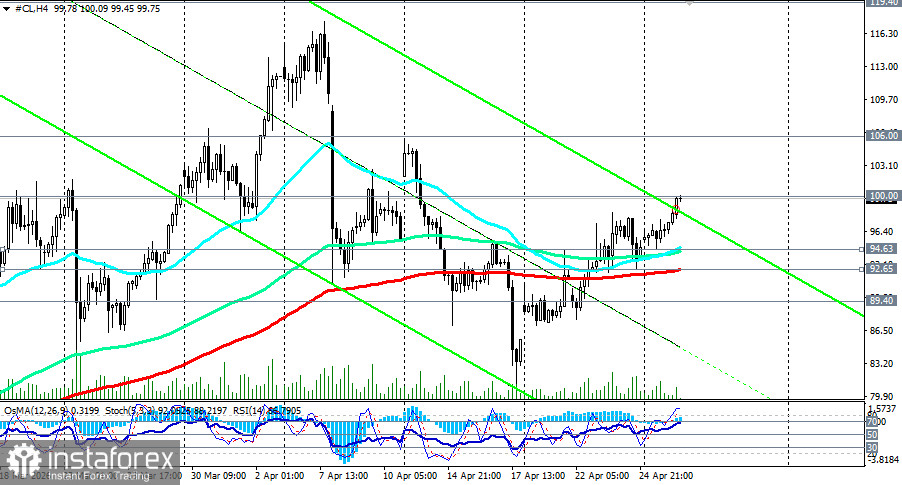

Technically, WTI confirms a strong upward impulse that began two weeks ago.

Price has firmly closed above the 50-period EMA on the 1-hour, 4-hour and daily charts (96.54, 94.63, 89.40 respectively), which is an early sign that the bulls have taken short-term control.

The 14-day RSI ranges between 55–58, indicating sustained upward momentum without signs of overbought conditions. This leaves room for further gains.

A break above the round level of 100.00 would likely open the door to new highs.

In short, the path of least resistance is up. Any local pullbacks will be treated by the market as buying opportunities ahead of the next leg higher.

Key events

- 29 April: US Congressional vote on the "War Powers Resolution" — could limit or expand the administration's authorities in the conflict with Iran, triggering volatility.

- 29–30 April: meetings of the Fed, ECB and Bank of England — rate decisions will affect the dollar and global energy demand outlook.

- This week: weekly API and EIA inventory reports — further US stock draws are expected, supporting prices.

Conclusion

The oil market has switched from hopes for a ceasefire to a regime of real physical shortage. The diplomatic process is frozen, and economists now expect normal flows through the Strait of Hormuz to resume no earlier than late May, and possibly later.

A technical break of the local resistance zone 100.00–100.40 would be a powerful signal for the rally to continue, opening the way to the $105.00–$110.00 range and beyond.

At the same time, the Suez Canal, the Bab-el-Mandeb strait and other routes remain vulnerable. If the conflict spreads to major Saudi shipping lanes, we could see prices exceed historic records. For now, the path of least resistance for WTI points above $100.00.